April 2026 US Nonfarm Payrolls Beat Forecasts as Labor Market Shows Signs of Cooling

The April 2026 US nonfarm payrolls report beat expectations, but weak wage growth, low labor force participation and soft working hours suggest the US labor market is still losing momentum.

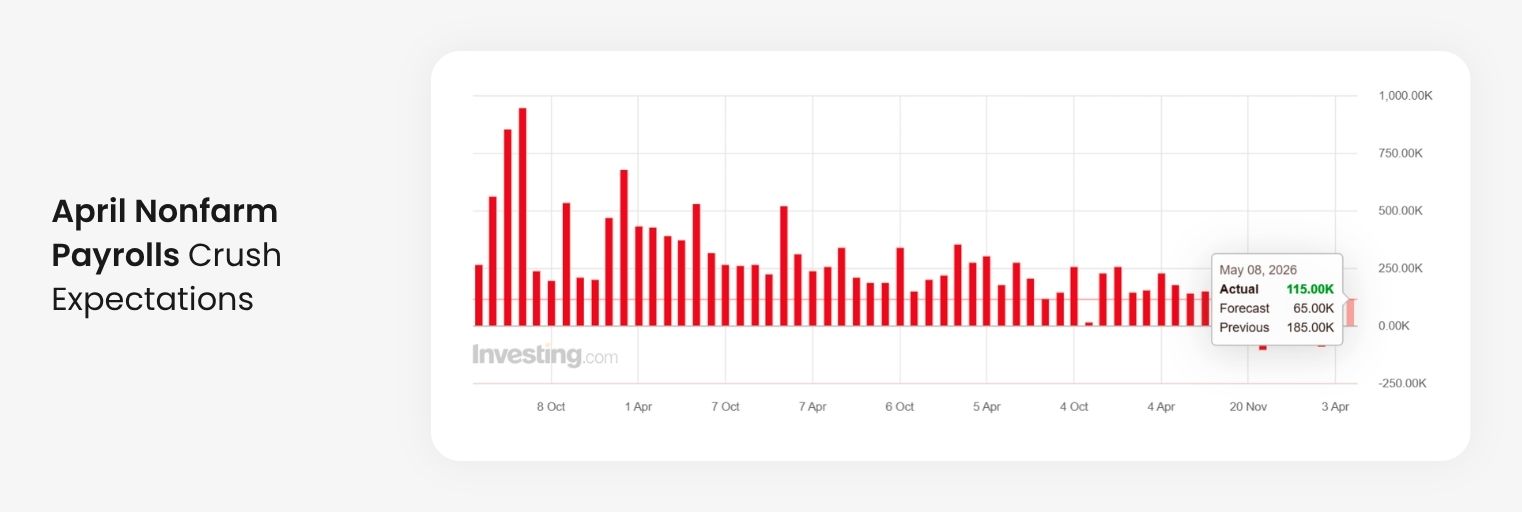

The April 2026 US nonfarm payrolls report gave markets a surprise.

The headline number came in better than expected:

Nonfarm payrolls: +115,000

Forecast: +65,000

Unemployment rate: 4.3%

Average hourly earnings: +3.6% YoY, below expectations

Average weekly hours: 34.3

At first glance, this looks like a decent US jobs report.

More jobs than expected. Unemployment still contained. No labor market collapse.

But traders know the headline number is only the first layer.

Under the surface, the April 2026 NFP report looks more mixed. Job growth beat forecasts, but wage growth slowed, labor force participation stayed weak, and working hours remained soft.

Is the US economy still strong enough to delay Fed rate cuts?

Let’s break it down.

Key Takeaways from the April 2026 US Nonfarm Payrolls Report

The April 2026 US jobs report was not clearly strong or weak. It was mixed.

Main takeaways:

Payrolls beat expectations at +115,000.

The unemployment rate stayed at 4.3%.

Wage growth slowed to 3.6% YoY.

Labor force participation remained weak at 61.8%.

Average weekly hours stayed low at 34.3.

The Fed may stay patient on rate cuts.

Market volatility could remain elevated.

In short:

The US labor market is not booming. But it is not breaking either.

That puts traders in a tricky zone.

April 2026 US Jobs Report: Payrolls Beat Forecasts, but Momentum Is Slowing

The biggest surprise was payroll growth.

The US economy added 115,000 jobs in April 2026, well above the 65,000 forecast. That suggests employers are still hiring, even as the broader economy slows.

April 2026 US nonfarm payrolls rose by 115,000, beating expectations of 65,000.

Recent labor data still points to cooling momentum:

March payrolls: +178,000

Three-month average: around 48,000

The three-month average remains subdued due to earlier weakness and revisions. So while April beat expectations, it does not mean the labor market is suddenly strong again.

A better read is this:

The labor market is weak, but resilient.

That matters for the Federal Reserve and for traders watching the US dollar, bond yields and equity indices.

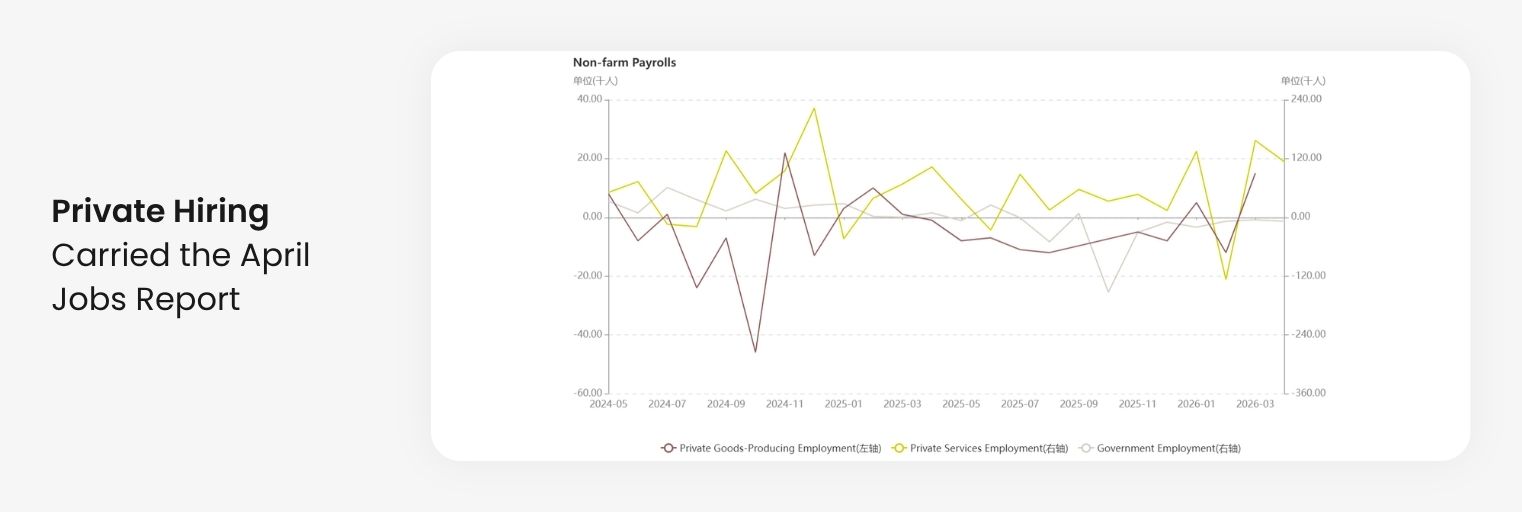

Private Hiring Is Carrying the Labor Market

Private hiring carried the April 2026 jobs report, while government payrolls declined.

Services are still doing most of the heavy lifting. But the pace is not strong enough to signal a major growth rebound.

For traders, the message is clear:

The labor market still has a pulse, but it is not running hot.

Labor Force Participation Remains the Weak Spot in the US Labor Market

If payrolls beat expectations, why does the labor market still feel soft?

US labor force participation remained weak in April 2026, signaling deeper softness beneath the headline jobs data.

Because the labor force participation rate remains weak.

Participation rate:61.8%

Still below the critical 62% level

These metric matters because it shows the share of people who are either working or actively looking for work.

Unlike the unemployment rate, labor force participation captures deeper trends such as:

retirements

discouraged workers

people leaving the labor force entirely

health or caregiving pressures

demographic shifts

Demographics Are Becoming a Structural Problem

One key issue is aging. Workers aged 55 and older continue to leave the workforce, while under-55 participation remains much stronger at 83.8%.

This creates a structural problem. Companies may want experienced workers, but many older workers are retiring permanently. That reduces long-term labor supply and can limit future economic growth.

In other words, the US economy may need to rely more on productivity, automation and AI-driven investment, not just more workers.

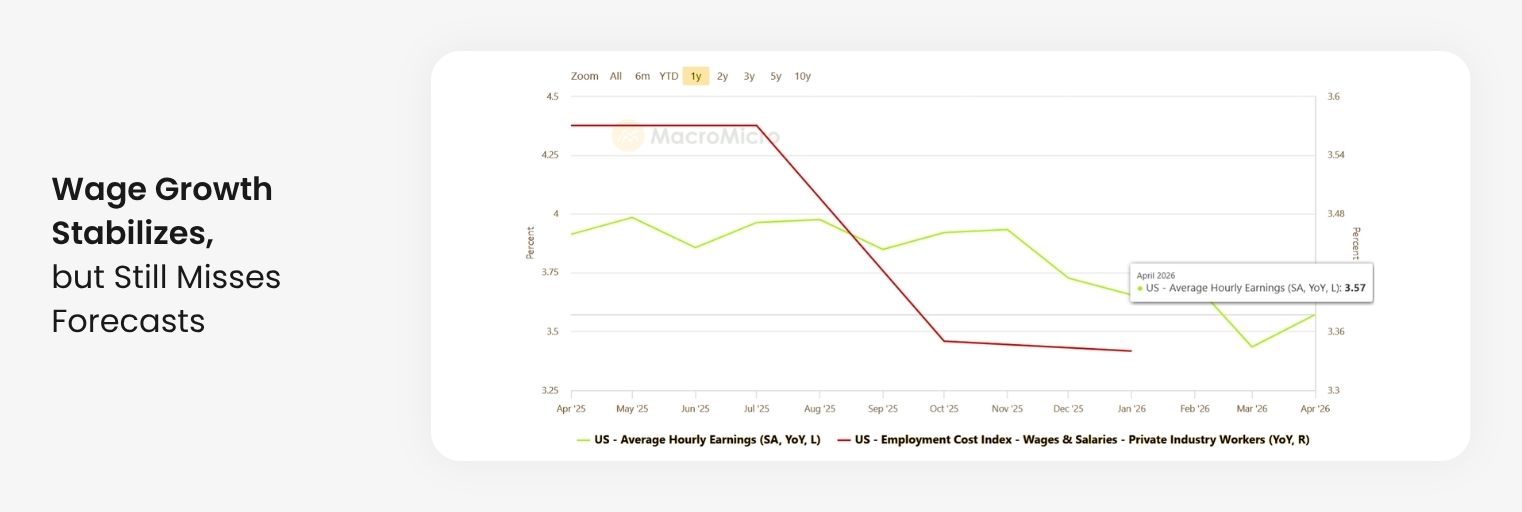

Wage Growth and Working Hours Point to Softer Consumer Demand

Wage growth is a big deal because consumer spending drives the US economy.

US wage growth slowed in April 2026, adding to signs of softer consumer income momentum.

Some sectors still saw stronger wage gains, including:

transportation and warehousing

construction

But overall, wage growth is not strong enough to suggest a major rebound in consumer spending.

Working hours tell the same story.

Average weekly hours stayed at:

34.3 hours

This is still relatively low. Businesses often reduce hours before they cut jobs, so soft working hours can be an early sign of weaker demand.

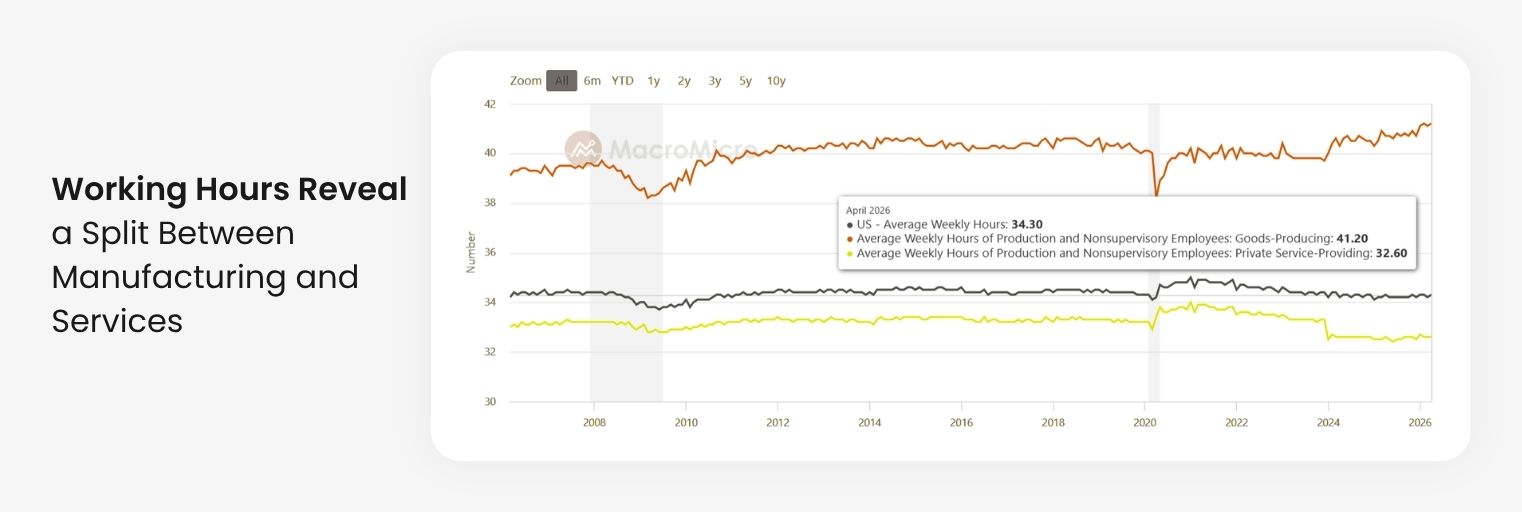

Manufacturing and Services Are Sending Different Signals

Manufacturing is still getting support from the AI infrastructure cycle. Investment in chips, data centers, automation and power infrastructure is helping stabilize parts of the economy.

Some factories are still relying on overtime work.

Services look softer.

US average weekly hours remained soft in April 2026, suggesting labor demand is stable but not strong.

This may reflect weaker demand, slower consumer activity or early efficiency gains from automation and AI.

This split matters. Manufacturing may stay supported by AI investment, while services may feel more pressure from weaker demand.

For traders, that means macro data could stay messy. And messy data usually means more volatility.

Why Consumer Spending Could Stay Weak

Based on current market conditions, it seems that US consumer market may remain sluggish in the near term.

The April 2026 US nonfarm payrolls report showed that hiring is still positive, but the income side of the story remains less convincing.

The main pressure points are:

Wage growth is stabilizing but still weak

Working hours remain soft

Inflation continues pressuring households

Overall income growth is simply not strong enough to drive a major rebound in spending.

Manufacturing, supported by the AI infrastructure boom, continues to stabilize the labor market through overtime work and investment activity.

The service sector tells a different story.

Working hours remain comparatively soft, potentially reflecting weaker demand and the early effects of AI-driven efficiency gains.

This growing divergence between manufacturing and services may become an increasingly important theme for the US economy in the quarters ahead.

For traders, this is worth watching. If consumer demand stays weak, markets may start paying more attention to retail sales, earnings guidance, credit data and consumer confidence.

Fed Rate Cuts in 2026: Why the Fed May Stay on Hold

The labor market is not collapsing.

But it is not overheating either.

That puts the Federal Reserve in a difficult position.

The Most Likely Outcome: Wait and See

This jobs report, combined with:

recent FOMC messaging

cautious Fed commentary

persistent inflation risk

supports one conclusion:

👉 The Fed is likely to stay on hold in 2026.

The Labor Market Is Reaching Balance

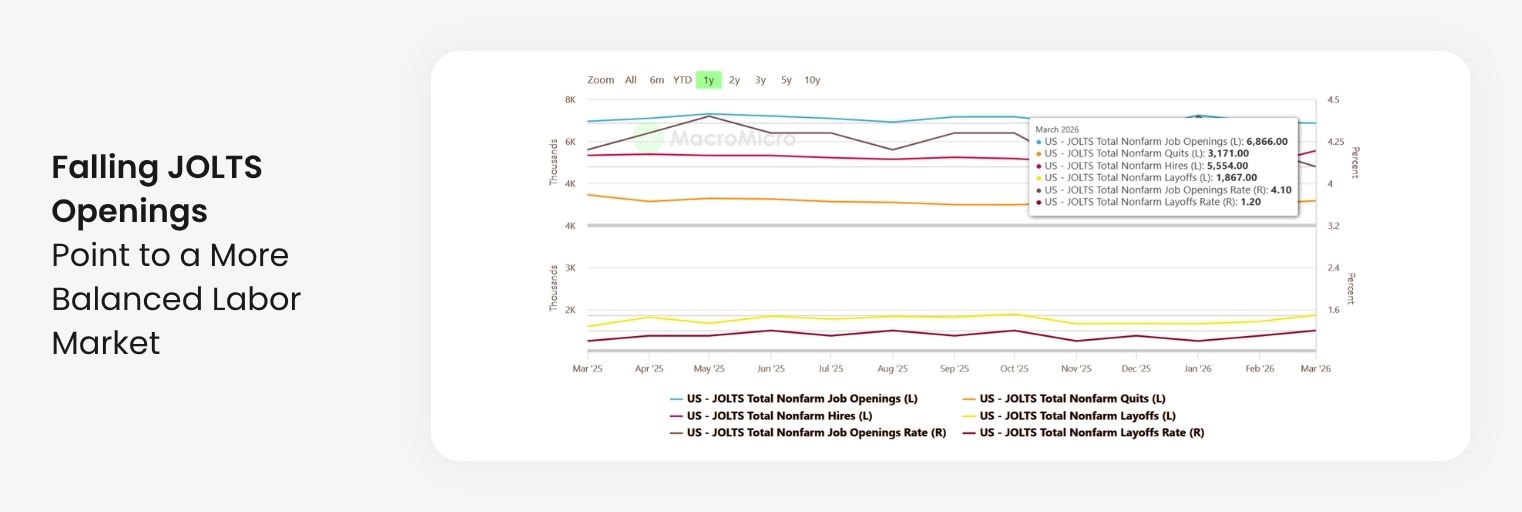

Another key signal comes from JOLTS job openings.

Job openings rate fell to 4.1% in March

This suggests that labor demand and supply are gradually moving into balance.

The Fed may see this as confirmation that the current policy is restrictive enough.

US JOLTS data showed the job openings rate falling to 4.1% in March 2026, pointing to a more balanced labor market.

Productivity Is Becoming More Important Than Labor

A major shift is happening beneath the surface.

Labor force growth is slowing.

As a result, the economy may increasingly depend on:

👉 productivity growth instead of labor expansion.

Q1 GDP data already points in this direction.

Investment, especially AI and infrastructure spending, has become the main growth engine.

Large technology companies continue investing aggressively in:

AI infrastructure

data centers

automation

This may help cushion the economy even if hiring weakens further.

The Bar for Rate Hikes Is Also Rising

At the same time, the Fed is unlikely to raise rates aggressively.

Oil and gas prices remain elevated as tensions around Iran and the Strait of Hormuz continue.

But policymakers appear cautious.

Recent Fed commentary suggests most officials prefer to:

monitor inflation carefully

avoid reacting too quickly

Even if inflation rises temporarily, the Fed is more likely to wait than immediately tighten further.

What the April 2026 NFP Report Means for Markets

The April 2026 nonfarm payrolls report looks strong on the surface.

But underneath, the US economy still appears soft.

Key signs of weakness include:

Hiring is slowing

Wage growth remains limited

Labor participation is weak

Consumer spending lacks momentum

At the same time:

the labor market is stable enough to avoid immediate rate cuts

inflation risks remain elevated

This leaves the Fed in a holding pattern.

For traders, this mixed setup could keep the US dollar, gold, stocks and Treasury yields sensitive to incoming data.

A stronger payroll headline may support the US dollar and yields if markets expect the Fed to keep rates higher for longer. But softer wage growth and weak participation could limit upside if traders start pricing future Fed rate cuts.

Gold may remain choppy as traders balance Fed policy, dollar strength and geopolitical risk. Stocks may also stay volatile, especially if weak consumer momentum weighs on earnings expectations.

In short, this is not a clean market signal.

It is a mixed report.

And mixed reports usually create messy price action.

👉 Volatility is likely to remain high.

Final Insight: April 2026 US Labor Market Is Transitioning

The April 2026 US nonfarm payrolls report shows a labor market that is no longer booming.

But it is not breaking either.

It is transitioning.

And in today’s market, that may be enough for the Federal Reserve to stay patient, even as inflation and geopolitical risks continue to rise.

Disclaimer

The information contained herein is provided for general informational and educational purposes only and does not constitute investment advice, financial advice, trading advice or any other form of professional advice, a recommendation, or an offer or solicitation to buy or sell any financial instruments or engage in any trading strategy.

Trading in leveraged products such as contracts for difference (CFDs) involves a significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Any references to market trends, asset performance, price levels, or forward-looking statements reflect opinions or general market commentary as at the date of publication and are subject to change without notice.

This article does not take into account any individual investor’s objectives, financial situation, or risk tolerance. Readers should conduct their own independent research and seek professional advice before making any investment or trading decisions. D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained herein. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.